You as long as the %rate is diff between lending and deposit rate, also should be principal time money multiplier minus 1, but yeh, bang on, they do get good mileage.Originally Posted by Brian d marge

111000101000100010011110

111000101000100010011110

You as long as the %rate is diff between lending and deposit rate, also should be principal time money multiplier minus 1, but yeh, bang on, they do get good mileage.

"A shark on whiskey is mighty risky, but a shark on beer is a beer engineer" - Tad Ghostal

Aio ki te Aorangi

From 100 of total deposits the banks end up with 457.05 of total deposits. Banks lend from deposits, coz that's exactly what the bank did when it had 100 to begin with. At that point in time there was also no money in circulation either. The bank has created 357.05 (assuming that the 100 wasn't printed out of thin air in the first place) from thin air and it has only been backed by 100. The only reason they have the likes of reserve/capital requirements is because it'd be obvious to joe public that they're creating money out of nothing.

I didn't think!!! I experimented!!!

God's Evil Twin

Here maybee pictures will help you to learned

Science Is But An Organized System Of Ignorance"Pornography: The thing with billions of views that nobody watches" - WhiteManBehindADesk

Bogeyman

It may be horseshit here in stupid world but I can assure you it's a perfectly correct and accurate summary of recent historical trends in the real world.

If you want to use real world arguments then bring numbers or stfu.

Trying to pretend that the current generation is worse off than any previous generation in any regard that matters is a function of fuckwits that desperately need to offload the blame for their own failure onto someone/thing else. It's bullshit, pure and simple.

Go soothingly on the grease mud, as there lurks the skid demon

KB's Chief Cats

no, no it isn't. you poor, poor, old, white cunt.

111000101000100010011110

Yeh, but that is a meaningless figure as it only counts money going in, it is the difference that matters. I can put the same 20buck note into my wallet 5 times but that doesn't give me 100bucks to spend, because after the first time I have to take it out again before putting it back it, which is why the bank has 357 of withdrawals to offset those deposits; it has no more created 357 than I can create $80 out of thin air with just a wallet and a bill.

Notice in that example the total loaned at each step gets smaller, total loaned overall is principal/reserve rate in your own example (100/0.1=1000=100+90+81+72.9+65.6....), thus contradicting your earlier point about $1 turning into $125 with a 20% reserve rate; so I put it to you, will the picture help you to learned? cos it backs up my point perfectly.

Also why did they omit that the 90 units is deposited again? in that example 100 units becomes 190 deposited and 171 loaned, or a net deposit of 19 unit with 81 remaining in circulation (ignoring the final arrow ofc); the sum still adds to 100 so what has actually been created?

"A shark on whiskey is mighty risky, but a shark on beer is a beer engineer" - Tad Ghostal

Royal Enfield user

Keep the 5 dollars in ya pocket write an iou 5 time and lend those out at5 percent

"Look, Madame, where we live, look how we live ... look at the life we have...The Republic has forgotten us."

Aio ki te Aorangi

Where does that money going in come from? Other than from it being lent out? Literally plucked out of thin air i.e. magic? after all, that 300-500 is more than the 100 it started out as.

111000101000100010011110

The original 100 goes in, then 80 is lent out, providing 80 that can come back in, etc etc, nothing is plucked from thin air. All the sums add up. Just like balancing a bank statement, you take both the income (deposits) and expenses (withdrawals) to find out how much money you actually have.

Or another example, me and 4 mates pass a 20 dollar note from wallet to wallet (0% fractional reserve), how has $80 been created and where is it?

"A shark on whiskey is mighty risky, but a shark on beer is a beer engineer" - Tad Ghostal

Bogeyman

I ain't poor, I ain't old and I ain't white.

And you're batting average ain't improving.

Like I said, numbers or stfu.

Go soothingly on the grease mud, as there lurks the skid demon

KB's Chief Cats

oh youre poor alright.

Bogeyman

A relative term, to be sure.

But I have everything I want.

Which, given your repetitive bleating about shit makes me relatively a fucking sight better off than you.

Akzel needs to work, (harder)

Go soothingly on the grease mud, as there lurks the skid demon

Royal Enfield user

The NZ banks as I understand them

First off NZ has no fractional reserve rate , As far AS I know . this mean it can lend out that dollar as much as they want ...

However they are constrained by capital requirement ratios. or capital adequacy ratio of around 76 % ( asb)

The governments or RBNZ prints around 2% in hard currency M1 cash ( off top of head )

New money enters the system by the RBNZ either by direct printing , ( yes hitting a few keys on a keyboard ) or selling of assets such as bonds , gold silver etc .... and they are constrained to hold the inflation rate between 2 AND 3% SO THEY CAN JUST INCREASE THE MONEY SUPPLY , so they go in the back door by allowing the reserve currency to accumulate interest.( cant find info on this about nz ) ...this is what QE actually is ......moving money so that it can be used .....

The banks now have capital to lend against, so

when you come in for a dollar ....they hit a few keys and produce out of thin air ...one dollar

at 5.75 %

So as there is no reserve to be kept , but are constrained by capital adequacy , 7.6% we get

Future value = $ 1 principle sum x 7.6 times they can lend it out x ( 1+ interest rate 5.75 ) ^no of years

Fv = 7.6 x ( 1+5.75 ) ^1

Fv= $9.50

now after the 1 year they have $8.37 to lend out .......NOT 7.6 compounding ,,,

therefore

FV= 8.37 x7.6 x (1+5.75)^1

=67.26

and so on .............540 ...$ 4339.98 .......$34 880........ $280 333.7.................

Now Im not sure how to apply the capital adequacy ratio I THINK it acts in the same way was the fractional reserve rate , which I think is 9 in America

So , if some one more knowledgeable could add , Im all ears , but them the facts as I understand them

Stephen

at the end of the day shonkey shylock was an apt description

at the current rate of 5.7 % per anumn

"Look, Madame, where we live, look how we live ... look at the life we have...The Republic has forgotten us."

Royal Enfield user

you look pretty peaky in ya picture , maybe its just a too high ISO setting .....

Stephen

"Look, Madame, where we live, look how we live ... look at the life we have...The Republic has forgotten us."

Royal Enfield user

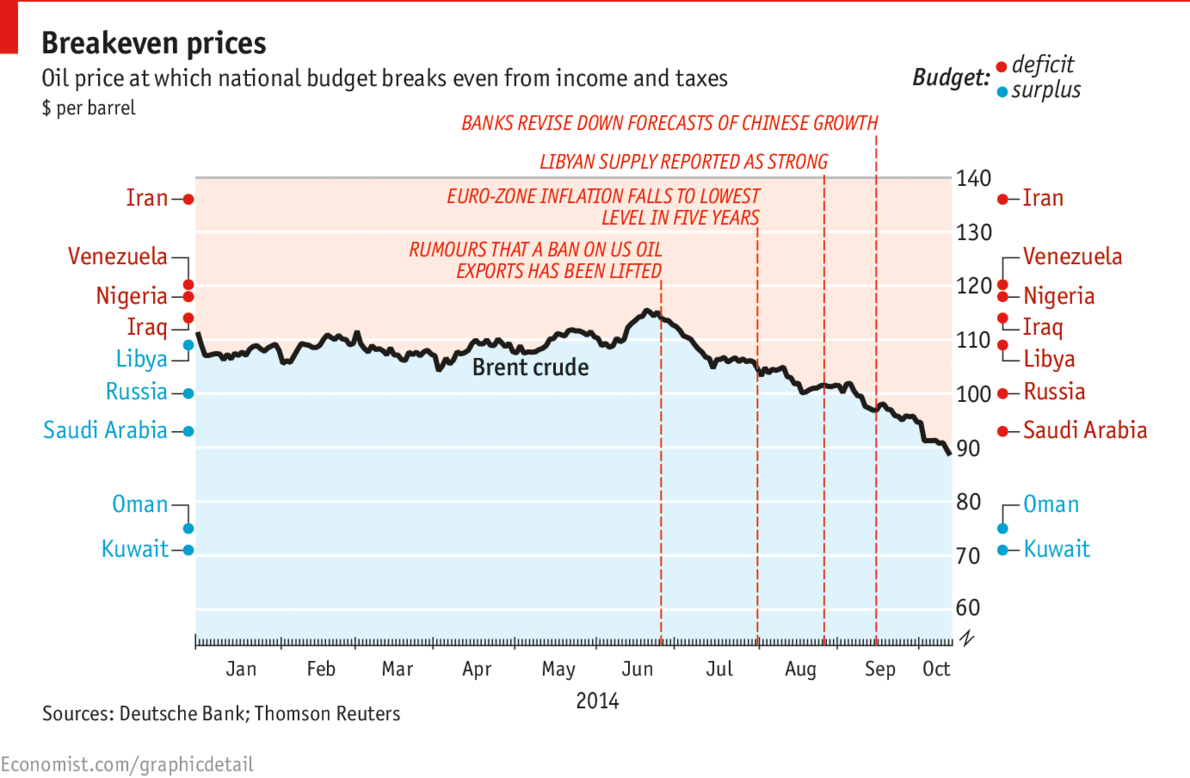

and as for who is dumping the oil .....

our friends the Saudis ......

"Look, Madame, where we live, look how we live ... look at the life we have...The Republic has forgotten us."

There are currently 59 users browsing this thread. (0 members and 59 guests)

Posting Permissions

Posting Permissions

Reply With Quote

Reply With Quote

Bookmarks